May 25, 2025 Letter to Clients

As we write this first letter of 2025, the first under a new administration in Washington, we want to express our gratitude for your patience in receiving this communication. As you can imagine, the first few months of this year have kept us especially busy, with much of our time dedicated to navigating the market and economic shifts taking place. In this letter, we aim to address key topics currently shaping the financial landscape and share our perspective on these developments.

Politics & Markets

Politics is a polarizing topic, which is why we choose to remain neutral when managing investments, basing decisions on solid, factual economic data and sound fundamentals. We will always respect the diversity of perspectives, beliefs and values among our clients, however as financial advisors, we also recognize the significant influence politics can have on global markets—especially in the short term.

We are currently seeing this dynamic play out, driven by ongoing trade tensions and the unpredictable, at times conflicting or speculative, information emerging from Washington. These factors, combined with growing investor sensitivity to any signals that might suggest political pressure on the Federal Reserve or attempts to compromise its independence—especially in light of President Trump's public criticism of Federal Reserve (the Fed) Chair Jerome Powell—are contributing to heightened market uncertainty.

The Federal Reserve: Independence is Critical

A recent headline dominating the news is President Trump’s dissatisfaction with the interest rate policy decision making by Jerome Powell, who he appointed to the position of Fed Reserve Chair in 2018. Previously, President Trump has suggested that the President should have influence over Federal Reserve policy, and this has raised concerns about the potential politicization of the Fed, an institution known for its independence in setting monetary policy. This scenario provides another example of the swift market reaction to developing news, announcements, and offhand remarks coming out of Washington.

To shed some light on why the markets would have such a strong and swift reaction to the President’s statements, which originally had investors concerned over potential political interference with the Fed’s independence, and the positive market reaction when the President offered comments that somewhat eased those investor concerns, we would like to offer an explanation of the autonomy of the Federal Reserve and the importance of its independence.

The Federal Reserve’s independence is a cornerstone of its ability to conduct effective monetary policy. It was designed to operate independently from short-term political pressures so it can make decisions that are in the long-term best interest of the economy, even if those decisions are unpopular. This independence allows the Fed to focus on its dual mandate—promoting maximum employment and maintaining stable prices—without interference from elected officials who may be motivated by political or electoral considerations.

Concerns arise when there is any indication that the Fed’s independence could be compromised. If political leaders were able to influence interest rate decisions or other policy actions, it could undermine investor confidence, lead to inflationary risks, and destabilize financial markets.

A politicized central bank might prioritize short-term gains over long-term economic health, which could erode the credibility of U.S. monetary policy and reduce the effectiveness of the Fed in managing economic cycles.

How We Began the Year and Where We Are Now

The market optimism that marked the beginning of 2025 has quickly faded. Initially fueled by hopes of sustained economic growth, interest rate cuts, controlled inflation, and deregulation under the Trump administration, investor confidence has since waned. Concerns of a potential recession or stagflation, the prospect of higher interest rates for an extended period, global unrest, and uncertainty about what might come next have all contributed to a more cautious and uneasy market sentiment.

This year the financial landscape has experienced extreme, notable shifts, particularly in the realms of trade policy and market reactions. As we are all very aware, one of the most impactful developments was the implementation of substantial tariffs on imported goods, which introduced a layer of unpredictability to the markets. The stock market, especially sectors with high foreign revenue exposure such as technology and industrials, has shown increased volatility.

The bond market is also navigating a complex environment. While some anticipate that the Fed may eventually lower interest rates in response to potential economic slowdowns, others express concerns about rising inflation and increased government debt, leading to a cautious outlook. Overall, the combination of aggressive trade policy and uncertain monetary responses has created a tense and unpredictable investment environment.

Tariffs: Impact To Stocks and Bonds

Under the new administration in Washington, the U.S. stock market has experienced notable volatility. Initially, the market responded positively to the President’s pro-business policies, including tax cuts and deregulation, which were anticipated to boost corporate profits and economic growth. This optimism led to significant gains in major indices like the S&P 500 and Nasdaq. However, with the announcement of aggressive tariff measures, the financial markets were rattled by the sweeping wave of new tariffs introduced by President Trump as part of his "Liberation Day" economic policy. These tariffs have raised concerns about inflation, supply chain disruptions, and retaliatory actions from trading partners, leading to increased market volatility and investor caution.

On April 2, the stock market reacted sharply to the tariff announcement. The Dow Jones Industrial Average (the Dow) plunged 1,679 points- the steepest single-day loss since March 16, 2020, when it plunged 2,997 points during the COVID-19 pandemic marking the largest point drop in history. While the Dow dropped 4%, the S&P 500 sank 4.8% and the Nasdaq 6%, it is important to note that the largest point gain of 2,963 points took place on April 9, 2025, only one week after the drop, reminding investors that historically some of the biggest point gains in the market follow the worst days and rewards those who remain steadfast. Over the following 48 hours after the tariff announcement, more than $6 trillion in market value was erased fueled by investor concern about how tariffs will impact corporate profits, global trade relationships, and inflation. While the long-term effects remain to be seen, the short-term reaction has been overwhelmingly negative as markets digest the risks of a trade war and potential economic slowdown.

Bond Vigilantes

Bond vigilantes is a phrase coined by economist Ed Yardeni in the 1980s to describe investors that had sold off scores of Treasury bonds to protest Federal Reserve policies they deemed too inflationary. A bond vigilante is a fixed-income trader who sells bonds or threatens to do so to push back against specific polices of the issuer, currently the U.S. government. While the stock market typically gets all the flashy headlines, cracks that appear in the bond market can be much more meaningful. While many investors are laser focused on the impact of the tariffs to the equities markets, it is likely the bond market that was the reason for President Trump’s pivot and temporary pause. Fixed income investors sent a message that the chaotic rollout of the tariffs had created uncertainty, more than investors were willing to tolerate. This is where the bond vigilantes stepped in and demanded higher yields as compensation for the risks they were being asked to take in the normally boring, risk-free, highly liquid U.S. Treasury market. The bond market shock can be attributed to several factors, some being fairly complicated such as the unwinding of a trade involving interest rate-based products, the fiscal chaos that is ensuing in Washington causing a significant decay of investor confidence, and highly leveraged hedge funds needing to raise cash quickly for operating income and to cover margin calls.

Initially, yields on shorter-term bonds rose as investors priced in expectations of higher inflation and interest rates due to tariffs. However, fears of a broader economic slowdown have since pushed long-term yields downward, signaling expectations that the Fed may have to cut interest rates later in the year to support growth. The 10-year Treasury yield briefly surged to 4.5%, a recent high—before easing as investors shifted toward safer assets.

Stagflation Concerns

Jerome Powell has warned that President Donald Trump’s trade tariffs could lead to higher inflation and slower economic growth — a troubling mix known as stagflation. Stagflation is an economic situation where three troubling things happen at the same time:

- Stagnant economic growth – The economy isn’t growing or is growing very slowly.

- High inflation – Prices for goods and services are rising quickly.

- High unemployment – A high number of people are out of work.

In a speech earlier this month, Powell stated, “The level of tariff increases announced so far is significantly larger than anticipated. The same is likely to be true of the economic effects.” He noted that the tariffs present a serious challenge for the Fed, which is responsible for keeping inflation low while also supporting job growth. If inflation rises while economic growth slows, the central bank could struggle to meet both of those goals at the same time. The last significant period of stagflation occurred in the 1970s and early 1980s with the key cause being a shock to oil prices due to geopolitical tensions and OPEC’s supply cuts. While there were concerns about stagflation during the post-COVID recovery, it proved to be more of a scare given that unemployment remained relatively low.

Staying The Course Does Not Mean “Set it and Forget it”

It's completely understandable to feel uneasy when markets turn volatile. You wouldn’t be alone in thinking about moving to cash and waiting until things "feel safer" before re-entering the market. Many investors have the same instinct, hoping to avoid losses and get back in once things start to rebound. But here’s where we want to offer some perspective. While the desire for short-term security is valid, stepping out of the market—even temporarily—can work against your long-term goals. Timing the market is extremely difficult, even for seasoned professionals, and some of the biggest gains often come during the early stages of recovery. Missing just a few of those strong days can make for a significant dent in overall returns.

The best and worst days often happen together and missing just a few good days could be very costly long term. We have put this statement in bold because of the significance we believe it holds. History shows us time and time again some of the best days in the market often follow the bad ones. The urge to sell investments to wait out the storm in cash is not uncommon, especially for retirees. The reasoning is typically that they can get back in once things begin to “settle down again” and they see the markets stabilizing. This desire for safety is certainly understandable and we recommend everyone have a healthy, liquid cash balance. Again however, history has shown us time and time again that the best days in the market often follow the bad ones and an investor can easily mistime their investment decisions and missing just a few of the good market days can be very costly over the long term.

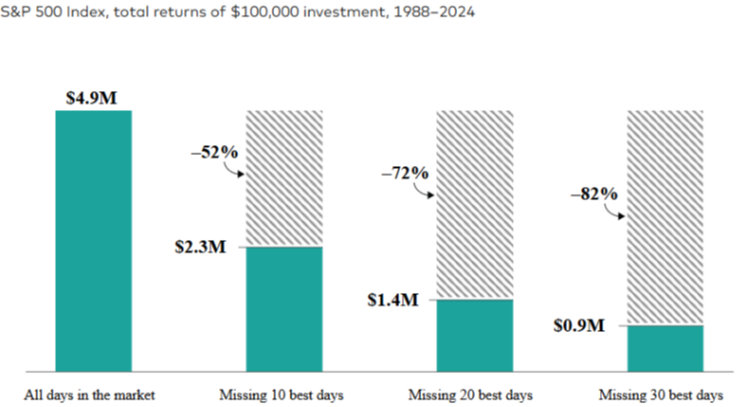

Here we illustrate a hypothetical $100,000 portfolio tracking the S&P 500 Index (starting in 1988), we can see the portfolio’s 2024 value if that money remained invested the entire time ($4.9 million), if it were out of the market for just 10 of the best-performing days ($2.3 million), if it had missed 20 of the best days ($1.4 million), and if it were out of the market for 30 of the best days ($0.9 million).

Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index. Source: Vanguard Investment Advisory Research Center calculated using data from Standard & Poor’s. As of December 31, 2024. Note: Return percentage calculated over a 37-year period: 11.1% = all days in the market, 8.9% = missing 10 best days, 7.3% = missing 20 best days, 6.0% = missing 30 best days.

Staying the course is a phrase that is often misunderstood as a passive strategy, akin to “buy and hold” or “set it and forget it”. In truth, staying the course requires thoughtful attention and active management. Much like a ship navigating toward a distant destination, even with a carefully plotted course, external forces can push it off track. To arrive at its intended destination, corrections and adjustments to account for outside forces must be made along the way. The same is true of your investment portfolio. Your asset allocation was built with your long-term goals and income needs in mind, considering your time horizon for the investments and your tolerance for risk. However, because different types of investments perform differently over time, your allocation will naturally shift with market movements. Part of our role is to monitor these shifts, take action when needed as well as take advantage of opportunities as they arise to best position portfolios. We do this process to make certain your portfolio remains aligned with the original strategy, ensuring it continues to reflect your goals and personal circumstances. For those with taxable accounts, there is actually a silver lining to market volatility – tax-loss harvesting. Tax-loss harvesting involves selling an investment that has declined in value, purchasing a similar investment, then claiming a tax deduction as a result. These losses can help offset capital gains and generate value. While opportunities are limited during steady market conditions, they often increase in more volatile periods, proving to be a silver lining.

In short, staying the course does not mean doing nothing—it means remaining committed to your plan and making the necessary adjustments to keep it on track, regardless of how markets behave in the short term. Communication is also key. We will continue to communicate with you and will actively reach out to those we identify as potentially requiring more significant portfolio adjustments based on their personal situation. From our clients, if your financial situation has changed since we last spoke, you anticipate either a major life change or significant expense on the horizon, please contact us to discuss it. We can review your portfolio and asset allocation to make sure your portfolio still reflects your current and future needs and objectives.

Our role is to help guide you through moments like these—to balance emotional, and very valid, reactions and concerns with sound strategy by using our expertise and many collective years of managing our client’s wealth through varying market conditions. Staying on course during turbulent times is never easy, but it can be one of the most powerful decisions you make for your financial future. As we have mentioned in previous letters during uneasy periods, we are committed to helping you effectively navigate this challenging market environment, and we welcome the opportunity to address any questions or concerns you may have or to simply chat about your financial situation so we may offer our expertise.

With all this said, thank you again for your patience on this first letter of 2025, and you can expect to continue to receive our correspondence as the year progresses. Lastly (but certainly not least), we are very pleased to welcome Natalya Pafumi to our firm as a Client Relationship Manager. Natalya joined us last month and is quickly becoming acclimated to her new role servicing our clients. Natalya has a demonstrated ability to provide exceptional service, and she looks forward to getting to know our clients personally. Welcome Natalya!

Sincerely,

Steve LePage Colleen Bianco